Job work is playing a very important role in the Indian economy. Job work means processing the raw material or semi-finished goods and covert into finished goods as required by the principal manufacturer. This concept was available in earlier law and also exist in in GST with special provision. The benefit of these provisions shall be available for the job worker and principal manufacturer both.

Meaning of GST Job work

As per section of 2(68) of the CGST Act, Job work means any treatment or process undertaken by person on goods belonging to another registered person (referred as Principal).

The one who does the said job would be termed as ‘Job Worker’. The ownership of goods does not transfer to job worker and ownership would be lying with Principal.

The Job worker will be carrying out the process as specified by the principal or owner of goods.

Advertisement

Content in this Article

Principal shall be registered person but job worker may be registered or un registered person.

Procedure Aspects related to Job work

A registered manufacturer can send the inputs (raw material or semi-finished goods) or capital goods without payment of tax with certain conditions to Job worker for further processing, repairing etc for as need of manufacture the intermediate or final products as case may be.

Principal can send the inputs or capital goods direct to job worker without bringing into his premises and can avail the credit of said inputs or capital goods.

Time Limit and Place for return of processed Goods

Principal can send the inputs or capital goods without payment of tax to job worker for further processing but after processing the goods within one year for inputs or three year for capital goods (other than moulds and dies, jigs and fixtures or tools) rare to be eturned or send to:

- Returned to the any place of the business of the principal

- Send to another job worker for further process.

- Remove the goods with payment to third party with in India or without payment in case of export in outside India but after the declaring his additional place of business of such job worker premises except in a case:

- Where the job worker is registered under the section 25 (mandatory registration) or

- Where principal is engaged in the supply of such goods as may be notified by the commissioner.

Principal shall send the inputs or capital goods to job worker through challan and challan shall contain the details as prescribed in invoice rules.

The responsibility of keeping books or accounts and other details laying with principal. [Section 143(2)]

Input tax credit on goods supplies to Job worker

Section 19 of CGST act provides that the principal can take the credit on inputs or capital goods sent to the Job worker. [Section 19(2) and (5)]

Deemed Supply [Section 143(3) and (4)]

Where inputs sent to the job worker for job work but not received back within the period one year of their being sent out, it shall be deemed that such inputs have been supplied by the principal to job worker on the day when inputs sent out the job worker. [Section 19(3) Where the inputs are sent directly to job worker, the period of one year shall be counted from the date of receipt of inputs by the job worker.

Where Capital goods sent to the job worker for job work but not received back within the period three year of their being sent out, it shall be deemed that such capital goods have been supplied by the principal to job worker on the day when capital goods sent out the job worker. [Section 19(6)] Where the capital goods are sent directly to job worker, the period of one year shall be counted from the date of receipt of capital goods by the job worker.

Section 19(3) and 19(6) are shall not be apply on the moulds and dies, jigs and fixtures or tool sent out to a job worker. [Section 19(7)]

Waste or Scrap Clearing Provision: [Section 143(5)]

- Waste generated at the premises of the job worker may be directly supplies by the registered job worker from his place of business with payment of tax. Or

- such waste or scrap may be cleared by the principal in case the job worker is not registered under the GST act.

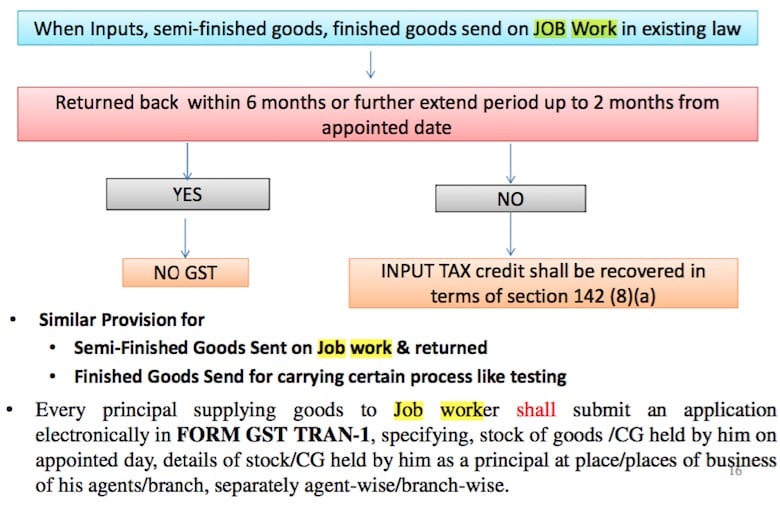

Miscellaneous Points (including amendment and clarification in circular No 88/07/2019 dated: 1st Feb 2019)

- Section 143 of the CGST act, 2017 vide section 29 of the CGST (Amendment) act 2018, empowering the commissioner to extend the return of the inputs and capital goods from the job worker. [one year in case of inputs and three year in case of capital goods]

- Responsibility of sending the goods for job work as well as bringing them back or supplying has been cast on the principal.

- Job worker is required to obtain the registration only in case where the aggregate turnover is exceeds threshold limit, whether the principal and job worker are located in same state or different state. (Exemption has been granted for interstate supply of services only).

- Value of mould and dies, jigs and fixture or tools received free of cost from the principal for the job work may not be included the value of job work service provided by the job worker because it will form part of the valuation of the principal for that particular supply.

- E-way bill is must be generated for interstate movement of goods without any monetary limit. (Rule 138 of the CGST act, 2017)

Recommended Articles

- GST Scope

- GST Return

- GST Forms

- GST Rate

- GST Registration

- What is GST?

- GST Invoice Format

- GST Composition Scheme

- HSN Code

- GST Login

- GST Rules

- GST Status

- Track GST ARN

- Time of Supply

If you have any query regarding “GST Job work Rules, Definitions, Procedure, Supply by Job Worker” then please tell us via below comment box…

In jwellery business if Urd coustmer give us old gold for making jwellery . We received labour when we make new jwellery. Is it job work? And what is gst rate on it?plz reply me.

In jwellery business if Urd coustmer give us old gold for making jwellery . We received labour when we make new jwellery. Is it job work? And what is gst rate on it?plz reply me.

In jwellery business if Urd coustmer give us old gold for making jwellery . We received labour when we make new jwellery. Is it job work? And what is gst rate on it?

In jwellery business if Urd coustmer give us old gold for making jwellery . We received labour when we make new jwellery. Is it job work? And what is gst rate on it?

Dear Sir,

We are manufacturer of Heavy Engg. m/c, in this procedure we have to sent the material for job work to job worker, some are registered , some are not registered in GST.

What would be the Impact if we get the work from UNREGISTERED.

1. WHO WILL PAY THE TAX ON JOB WORK CHARGES

2. HOW WE WILL TREAT HIS INVOICE IN OUR GST RETURNS.

Dear Sir,

We are manufacturer of Heavy Engg. m/c, in this procedure we have to sent the material for job work to job worker, some are registered , some are not registered in GST.

What would be the Impact if we get the work from UNREGISTERED.

1. WHO WILL PAY THE TAX ON JOB WORK CHARGES

2. HOW WE WILL TREAT HIS INVOICE IN OUR GST RETURNS.