How to identify the Category of goods under the new GST regime?Various states in India presently have their own systems for classifying goods for tax determination. However, for the purpose of uniformity in classification under the GST regime both at the National level and International level, it is desired to move to Harmonized System of Nomenclature (HSN) for goods and Services Accounting Code (SAC) system for services.

- HSN for goods

- SAC for services

The basis of HSN classification: HSN are arranged in order of product’s degree of manufacture or in terms of its technological complexity.

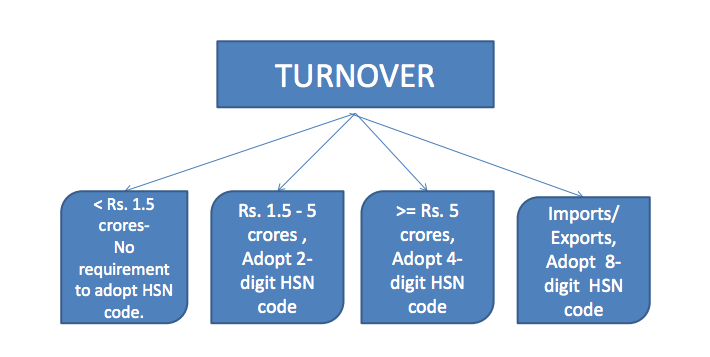

GST provides the dealers to adopt either two- or four- or eightdigit HSN codes for their commodities which is dependent on the turnover of the preceding year.

How to Identify the Category of goods under the new GST

Note: The 8- digit HSN code adopted for imports and exports have to be compatible to Global Standards.

Advertisement

Content in this Article

CLASSIFICATION RULES

- General Interpretative Rules (GIR) is applied for classification of a particular item in a sequential manner.

- On completion of classification, there is no need to continue applying the remaining Rules.

- Next rule is to be applied only if from the previous rule, the classification was not possible.

- Classification is final when there is no ambiguity or confusion.

Rule 1

- Titles of sections, chapters, and sub-chapters are provided for ease of reference only.

- For legal purposes, refer to headings and sub-headings to drive classification

Examples for Rule 1

1. If you were importing Christmas tree candles, it would seem logical to classify them with Classification Number 9505.10.00.90 – Other, articles for Christmas festivities. However, when reading the Notes to Chapter 95, it clearly states this Chapter does not cover Christmas tree candles. In fact, we must classify them with the Classification Number 3406.00.00.00 – Candles, tapers and the like.

2. Chapter 31 notes provides for certain heading 3102 3103 3104 consequently these heading cannot be extended to include goods which otherwise might fall there by reason. These heading cannot be extended to include goods which otherwise might fall there by reason.

Rule 2a

If the goods are incomplete/unfinished and have the characteristics of the finished product, classification is the same as that of the finished product (if the classification is known).

The heading shall also include removed/unassembled or disassembled parts

Examples for Rule 2a

- 1. An automobile missing only its wheels would be classified the same as if it were complete.

- 2. Railway coaches removed without seats would still be railway coaches.

- 3. A car without seats would still be classified as car.

- 4. Dismantled machinery in CKD/SKD will be classified as main machinery.

- 5. Scooter without engine will be classified as scooter.

Rule 2b

- Any reference to a material or substance includes a reference to mixtures or combinations of that material or substance with other materials or substances

- The classification of goods consisting of more than one material or substance shall take place as per Rule 3

Examples for Rule 2b

- 1. If you were importing dicalcium citrate, the Tariff does not specifically state this compound. However, it is a compound containing more than one material and its essential character is that of a salt of citric acid. Therefore, dicalcium citrate qualifies as Classification Number 2918.15.90.19: Salts and esters of citric acid, Other..

- 2. The term coffee will include coffee mixed with chicory.

- 3. Natural rubber will cover a mixture of natural and synthetic rubber.

- 4. Article of Gold includes articles partly made of Gold.

Rule 3a

Choosing a specific heading is preferred over a general heading

Example:

85.10 is the classification for “shavers, hair clippers and hair removing appliances, with self-contained electric motor.” This is a more specific classification for a handheld electric razor than:

67: “tools for working in the hand, pneumatic, hydraulic or with self-contained electric or non-electric motor,” or

Examples for Rule 3a

- Mint tea is not stated specifically, as a product, in the Tariff. Although the product descriptions available are mint and tea, the importer must classify mint tea under the appropriate tea Heading because it provides the most specific product description and mint is only the flavour of the tea.

- Heading 8510 covers Shavers and hair clippers with self contained electric motors. Heading 8509 covers electro magnetic domestic appliances with self contained electric motors. An electric Shaving Machine will be classified as 8510 which is the most specific description.

Rule 3b

Mixtures/composite goods should be classified per the material or substance that gives them their essential character

Example: a grooming kit consisting of electric hair clippers (85.10), a comb (96.15), and a brush (96.03) inside a leather case (45.02), should be classified under the electric hair clippers heading (85.10)

Examples for Rule 3b

1. An importer bringing in “liquor gift sets” (that include the bottle of liquor and glasses) must classify the goods under the appropriate liquor Heading. The essential character of the item is the liquor itself and not the glasses contained within the set.

2. Lead pencil with an eraser at the back: Though the above product is composite good, the essential character is that of a pencil and the attachment of eraser at the stub is added for convenience. Therefore, it will be classified as pencil.

Rule 3c

If two headings are equally suited to the item, choose the heading that appears last in numerical order.

Examples for Rule 3c

1. A gift set which includes socks (Heading number 6115) and ties (Heading number 6117) cannot be classified by the previous rule since neither item gives the gift set its essential character. The gift set must be classified under the Heading number for ties which is the Heading that occurs last in numerical order.

2. Electrical Insulating self adhesive tape can be classified as Electrical insulator 8546 or Self adhesive Tape 3919. Even though each of the headings is equally specific, by virtue of Rule 3(c), the last heading 3919 will be the appropriate heading for classification.

Rule 4

If goods cannot be classified per the above rules, they are to be classified according to the goods to which they are most akin

Examples for Rule 4

1. Plastic films used to filter or remove the glare of the sun light, pasted on car glass windows, window panes etc. These goods do not find a specify entry in the tariff schedule. However, heading 3925 30 00 covers Builder’s wares of plastic not elsewhere specified- shutters, blinds. Though the product in question is not builder’s ware, they are most akin to plastic binds and hence classified under this head.

2. Laddus made of sugar are imported. No tariff entry to cover them. The Akin goods are sugar confectionery chapter 17.

Rule 5

- Containers specifically designed for the article and suitable for long-term use will be classified along with that article, if such articles are normally sold along with such cases.

- Example: a camera case would fall under cameras.

- Packing materials and containers are also to be classified with the related goods except when the packing is for repetitive use

Examples for Rule 5a

1. Rule 5 (a) would apply to flute cases because flutes are normally sold with their cases (due to their specific shape) and are intended for long term use

Examples for Rule 5b

1. An importer bringing in goods and using styrofoam chips for padding fits well into Rule 5 (b). Styrofoam chips are normally used for the padding and insulation of many goods, however they are rarely reused and are therefore classified with the goods when they enter Canada.

2. Leather cases, which are normally supplied along with the goods, need not be treated separately for the purpose of classification.

Recommended articles

- GST Quiz

- GST Rules

- Returns Under GST

- GST Registration

- GST Rate

- GST Forms

- HSN Code List

- GST Login

- GST Software

- GST Suvidha Provider

- State GST Act

I am rexine two Wheeler’s seat covers MFG.MY turnover 30LACKS for year how pay the tax for yeat

I am rexine two Wheeler’s seat covers MFG.MY turnover 30LACKS for year how pay the tax for yeat