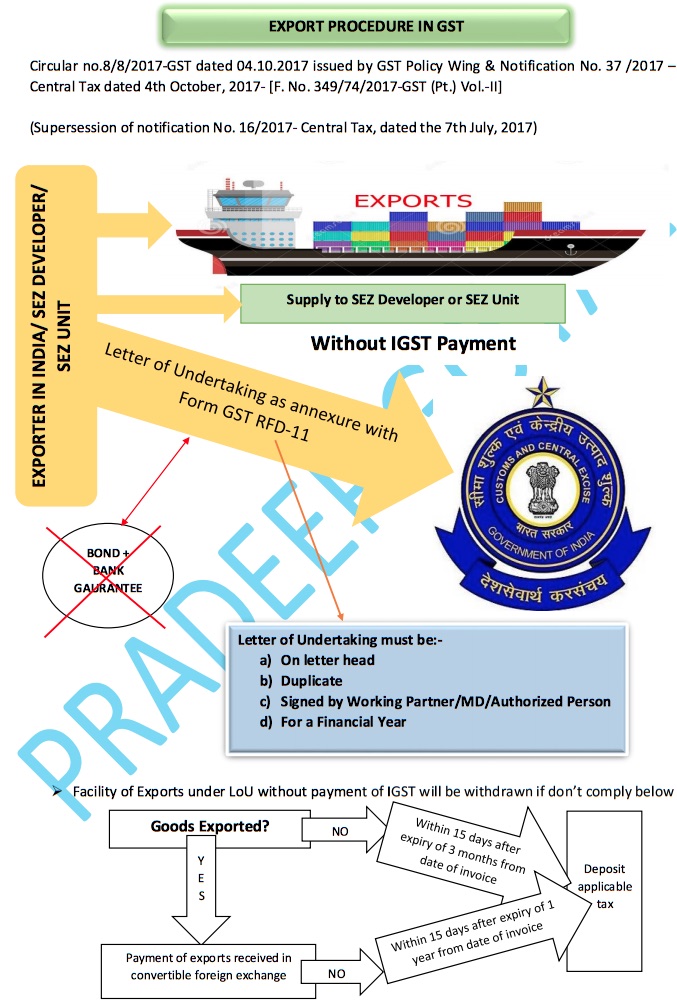

Revised Procedure for Exports in GST: Analysis of Export procedure with latest changes- Notification 37/2017-CT dated 04.10.2017 and Circular No. 8/8/2017-GST dated 04.10.2017 issued by GST Policy Wing.Notification No. 37 /2017 – Central Tax dated 4th October, 2017- [F. No. 349/74/2017-GST (Pt.) Vol.-II].(Supersession of notification No. 16/2017- Central Tax, dated the 7th July, 2017).

Revised Procedure for Exports in GST

Other Important Points

Three circulars in this matter, namely Circular No. 2/2/2017 – GST dated 5th July, 2017,

Circular No. 4/4/2017 – GST dated 7th July, 2017 and Circular No. 5/5/2017 – GST dated

11th August, 2017, which were issued for providing clarity on the procedure to be

followed for export under bond/LUT, are revised and a consolidated in this circular no.

8/8/2017-GST dated 04 October, 2017.

Eligibility to export under LUT

All registered persons who intend to supply goods or services for export without payment

of integrated tax except those who have been prosecuted for any offence under the CGST

Act or the Integrated Goods and Services Tax Act, 2017 or any of the existing laws and

the amount of tax evaded in such cases exceeds two hundred and fifty lakh rupees.

(Unlike Notification No. 16/2017-Central Tax dated 7th July, 2017 which extended the

facility of export under LUT to status holder as specified in paragraph 5 of the Foreign

Trade Policy 2015-2020 and to persons receiving a minimum foreign inward remittance

of 10% of the export turnover in the preceding financial year which was not less than Rs.

one crore).

Advertisement

Content in this Article

Documents for LUT

Self-declaration to the effect that the conditions of LUT have been fulfilled shall be

accepted unless there is specific information otherwise. That is, self-declaration by the

exporter to the effect that he has not been prosecuted should suffice for the purposes of

Notification No. 37/2017- Central Tax dated 4 th October, 2017. Verification, if any, may

be done on post-facto basis.

Time for acceptance of LUT

LUT will be accepted within a period of three working days of its receipt along with the

self-declaration as stated above by the exporter. If the LUT is not accepted within a period

of three working days from the date of submission, it shall deemed to be accepted.

Jurisdictional officer

LUT shall be accepted by the jurisdictional Deputy/Assistant Commissioner having

jurisdiction over the principal place of business of the exporter. The exporter is at liberty

to furnish the LUT before either the Central Tax Authority or the State Tax Authority till

the administrative mechanism for assigning of taxpayers to the respective authority is

implemented.

Author –Pradeep Goyal

Recommended Articles

- Exports under GST

- Section 147 of GST

- Important Questions

- GST on Imported Goods

- GST Rates 2017