Delivery challan under GST: The principal can send goods for further processing or capital goods to the job worker under the cover of challan issued by the principal. Challan must be issued by the principal even for inputs and capital goods directly send to the job-worker. Job work challan must conform to the GST invoice rules and the responsibility for keeping proper accounts as per GST requirements would lie with the principal.

Delivery Challan Format

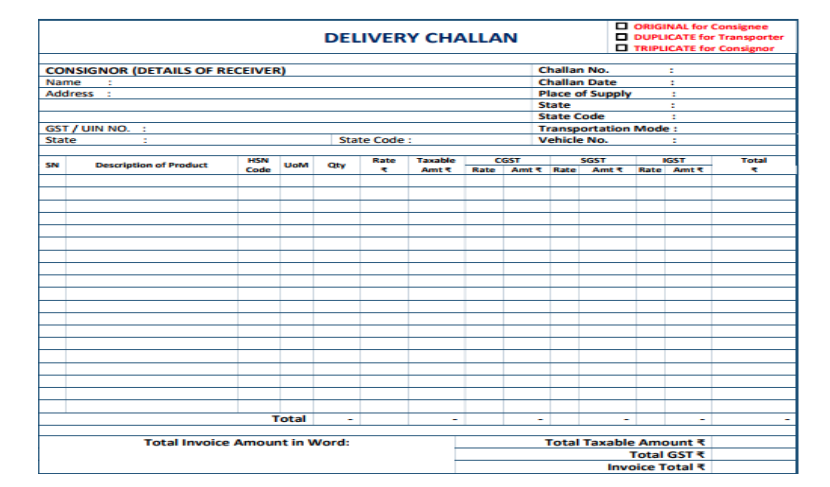

A delivery challan should be serially numbered not exceeding 16 characters, in one or multiple series, in lieu of invoice at the time of removal of goods and should contain the following details :-

- Delivery challans must be serially numbered not exceeding sixteen characters, in one or multiple series. The following information must be mentioned in all delivery challan formats:

- Date and number of the delivery challan.

- Name, address and GSTIN of the consigner, if registered.

- Name, address and GSTIN or Unique Identity Number of the consignee, if registered. If unregistered, name, address and place of supply.

- HSN code for the goods.

- Description of goods.

- Quantity of goods supplied (provisional, where the exact quantity being supplied is not known).

- Taxable value of supply.

- GST tax rate and tax amount broken down as CGST, SGST, IGST and GST Cess – where the transportation is for supply to the consignee.

- Place of supply, in case of inter-state movement of goods.

- Signature.

DownloadDelivery challan format

Certain Provisions relating to job work

Section 143(1) read with section 19(1) of the CGST Act,2017 provides that a registered person may send any inputs/ capital goods without payment of tax to a job worker for job work (under the cover of delivery challan) and the principal shall subject to certain conditions and restrictions be allowed Input Tax Credit (ITC) on inputs sent to a job worker for job work.

It is pertinent to mention that in terms of Section 19(2) and 19(5) of CGST Act, 2017, the principal can also send goods directly to the place of job worker without receiving the said goods in his premises first and ITC can also be availed in such cases though the principal has not received the goods.After job work, goods may be sent to another job worker or may be brought back to any of the place of business of the manufacturer (under delivery challan). The manufacturer is not required to reverse the credit or pay tax on supply of said inputs/ capital goods.

Advertisement

Recommended Articles

- Time of Supply GST

- FAQ on Time of Supply

- GST Rules

- Place of supply

- GST Registration

- GST Rates

- Time of Supply

- GST Downloads

- GST Forms

Very useful website. keep it up. Best wishes

Very useful website. keep it up. Best wishes