AS 22 Accounting for Taxes on Income: The objective of this Standard is to prescribe accounting treatment of taxes on income. Taxable income may be significantly different from the accounting income posing problems in matching of taxes against revenue for a period.

Reasons:

- 1) Difference between items of revenue and expenses as appearing in the Statement of Profit and Loss and the items which are considered as revenue, expenses or deductions for tax purposes.

- 2) Difference between the amount in respect of a particular item of revenue or expense as recognised in the Statement of Profit and Loss and the corresponding amount which is recognised for the computation of taxable income

Differences between accounting income and taxable income

| Permanent Differences Differences that originate in one period and do not reverse subsequently | Timing Differences Differences that originate in one period and are capable of reversal in one or more subsequent periods |

Accounting income (loss) is the net profit or loss for a period, as reported in the Statement of Profit and Loss, before deducting income tax expense or adding income tax saving.

Taxable income (tax loss) is the amount of the income (loss) for a period, determined in accordance with the tax laws, based upon which income tax payable (recoverable) is determined.

Current tax is the amount of income tax determined to be payable (recoverable) in respect of the taxable income (tax loss) for a period.

Content in this Article

Deferred tax is the tax effect of timing differences.

Scope of AS 22

- Taxes on income include all domestic and foreign taxes which are based on taxable income.

- This AS does not specify when, or how, an enterprise should account for taxes that are payable on distribution of dividends and other distributions made by the enterprise.

Recognition

- Tax expense for the period, comprising current tax and deferred tax, should be included in the determination of the net profit or loss for the period.

- Deferred tax should be recognised for all the timing differences, subject to the consideration of prudence in respect of deferred tax assets (DTA).

- When there is unabsorbed depreciation or carry-forward of losses under tax laws – DTA should be recognised only to the extent there is virtual certainty supported by convincing evidence that sufficient future taxable income will be available against which such deferred tax assets can be realised. In other circumstances, DTA should be recognised only to the extent there is reasonable certainty that sufficient future taxable income will be available against which such deferred tax assets can be realised.

Definitions

- Tax expense (tax saving) – Current tax + deferred tax charged/ credited to statement of profit and loss for the period.

- Current tax – Income tax determined to be payable (recoverable) in respect of taxable income (tax loss) for a period.

- Deferred tax is the tax effect of timing differences.

- Timing differences – Differences between taxable income and accounting income for a period that originate in one period and are capable of reversal in one or more subsequent periods.

- Permanent differences – Differences between taxable and accounting income for a period that originate in one period and do n

Measurement

- Current tax should be measured at the amount expected to be paid to (recovered from) the taxation authorities, using the applicable tax rates and tax laws.

- Deferred tax assets and liabilities should be measured using the tax rates and tax laws that have been enacted or substantively enacted by the balance sheet date.

- Deferred tax assets and liabilities should not be discounted to their present value.

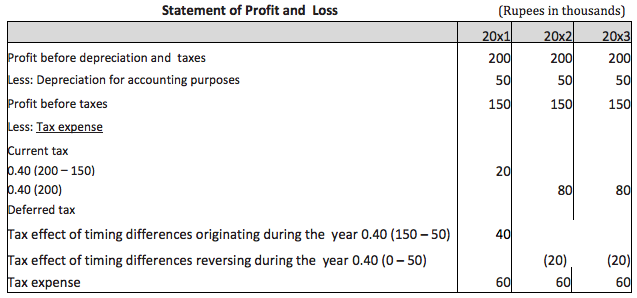

Illustration 1

On 1st April, 20×1, ABC Ltd. purchases a machine at a cost of Rs.1,50,000. Useful life of three years and an expected scrap value of zero. Although it is eligible for a 100% first year depreciation allowance for tax purposes, SLM is considered appropriate for accounting purposes. ABC Ltd. has PBDT of Rs.2,00,000 each year and the corporate tax rate is 40 per cent each year.

The following Journal entries will be passed:

Illustration 2 [rate of tax changes]

Advertisement

It would be necessary for the enterprise to adjust the amount of deferred tax liability carried forward by applying the tax rate that has been enacted by the balance sheet date on accumulated timing differences at the end of the accounting year. For example, if in Illustration 1, the substantively enacted tax rates for 20×1, 20×2 and 20×3 are 40%, 35% and 38% respectively, the amount of deferred tax liability would be computed as follows:

The deferred tax liability carried forward each year would appear in the balance sheet as under:

- 31st March, 20×1 = 0.40 (1,00,000) = Rs.40,000

- 31st March, 20×2 = 0.35 (50,000) = Rs.17,500

- 31st March, 20×3 = 0.38 (Zero) = Rs. Zero

Accordingly, the amount debited/(credited) to the profit and loss account (with corresponding credit or debit to deferred tax liability) for each year would be as under:

- 31st March, 20×1 Debit = Rs.40,00

- 31st March, 20×2 (Credit) = Rs.(22,500)

- 31st March, 20×3 (Credit) = Rs.(17,500)

Illustration 3 [Amounts in Rs.lakhs]

- PBDT for 15 years is Rs.1000 per year, both as per the books of account and for in- come-tax purposes.

- 100% tax-holiday for the first 10 years U/s 80-IA [or U/s 10A/10B]. Tax rate is assumed to be 30%.

- At the beginning of year 1, the enterprise purchased one machine for Rs.1500. Residual value is nil.

- For accounting purposes, enterprise follows SLM policy for depreciation on machine over 15 years.

- For tax purposes, depreciation rate relevant to the machine is 25% on WDV basis.

The following computations will be made, ignoring the provisions of section 115JB (MAT), in this regard:

At the end of 15th year, carrying amount of machinery for accounting purposes = nil, for tax purposes, Rs.19 lakhs which is eligible to be allowed in subsequent years.

Notes: 1. Deferred tax on timing differences which reverse during tax holiday [228] period should not be recognised. Timing differences which originate first are considered to reverse first. The reversal of timing difference of 228 during the tax holiday period, would be considered to be out of the timing difference which originated in year 1 [275]. The rest of the timing difference originating in year 1 [275-228=47] and timing differences originating in years 2 to 5 would be considered to be reversing after the tax holiday period.

Existence of unabsorbed depreciation or carry forward of losses under tax laws is strong evidence that future taxable income may not be available. Enterprise should recognises deferred tax assets only to the extent that there is other convincing evidence that sufficient taxable income will be available against which such DTA can be realised. The nature of the evidence supporting its recognition is disclosed.

Existence of unabsorbed depreciation or carry forward of losses under tax laws is strong evidence that future taxable income may not be available. Enterprise should recognises deferred tax assets only to the extent that there is other convincing evidence that sufficient taxable income will be available against which such DTA can be realised. The nature of the evidence supporting its recognition is disclosed.

Explanation [Para 17]:

- Determination of virtual certainty that sufficient future taxable income will be available is a matter of judgement based on convincing evidence and will have to be evaluated on a case to case basis.

- Example, Profitable binding export order, cancellation of which will result in payment of heavy damages by the defaulting party. On the other hand, a projection of the future profits made by an enterprise based on the future capital expenditures or future restructuring etc. submitted even to an outside agency, e.g., to a credit agency for obtaining loans and accepted by that agency cannot, in isolation, be considered as convincing evidence.

- PandL A/c – includes ‘loss’ which can be set-off in future for taxation purposes, only under ‘Capital gains’ – that item is timing difference to the extent not set-off in the current year and allowed to set-off against income arising under ‘Capital gains’ in subsequent years.

- The examples – sale of an asset giving rise to capital gain after balance sheet date but before financial statements are approved, and binding sale agreement which will give rise to capital gain (eligible to set-off the capital loss as per the provisions of the Act).

- Difference in ‘loss’ recognised for accounting and tax purposes because of cost indexation – in respect of long- term capital assets – DTA recognised and carried forward on the amount which can be carried forward and set-off in future years as per the provisions of the Act.

Re-assessment of Unrecognised Deferred Tax Assets

At each balance sheet date – Re-assess previously unrecognised DTA to the extent that it has reasonably or virtually certain, that sufficient future taxable income will be available against which DTA can be realised. Example, improvement in trading conditions.

- The payment of tax U/s 115JB = Current tax for the period.

- In a period where tax payable U/s 115JB, DTA and DTL measured using regular tax rates and not the tax rate U/s 115JB of the Act.

- When different tax rates apply to different levels of taxable income, DTA and DTL measured using average rates.

- Deferred tax assets and liabilities should not be discounted to their present value.

Illustration 4

From the following details of A Ltd. for the year ended 31 -03-2014, calculate the deferred tax asset/ liability as per AS 22 and amount of tax to be debited to the Profit and Loss Account for the year.

| Particulars | Rs. |

| Accounting Profit | 6,00,000 |

| Book Profit as per MAT | 3,50,000 |

| Profit as per Income Tax Act | 60,000 |

| Tax rate | 20% |

| MAT rate | 7.50% |

Solution

- Tax as per accounting profit 6,00,000 X 20%= Rs.1,20,000

- Tax as per Income-tax Profit 60,000 X 20% =Rs.12,000

- Tax as per MAT 3,50,000 X 7.50%= Rs.26,250

- Tax expense = Current Tax + Deferred Tax

- Rs.1,20,000 = Rs.12,000 + Deferred tax

Therefore, Deferred Tax liability as on 31-03-2014

= Rs.1,20,000 – Rs.12,000 = Rs.1,08,000

Amount of tax to be debited in Profit and Loss account for the year 31-03-2014

Current Tax + Deferred Tax liability + Excess of MAT over current tax

- = Rs.12,000 + Rs.1,08,000 + Rs.14,250

- = Rs.1,34,250

An enterprise should offset deferred tax assets and deferred tax liabilities if: It has legally enforceable right to set off and DTA and DTL relate to taxes on income levied by same governing taxation laws.

Transitional Provisions

For the purpose of determining accumulated deferred tax in the period in which this Standard is applied for the first time, the opening balances of assets and liabilities for accounting purposes and for tax purposes are compared and the differences, if any, are determined. The tax effects of these differences, if any, should be recognised as deferred tax assets or liabilities, if these differences are timing differences.

Example, in the year in which enterprise adopts this AS, opening balance of a fixed asset is Rs.100 for accounting purposes and Rs.60 for tax purposes. The difference is because the enterprise applies WDV method of depreciation for calculating taxable income whereas for accounting purposes SLM is used. This difference will reverse in future when depreciation for tax purposes will be lower as compared to the depreciation for accounting purposes. In the above case, assuming that enacted tax rate for the year is 40% and that there are no other timing differences, DTL of Rs.16 [(Rs.100 – Rs.60) x 40%] would be recognised.

Another example is an expenditure that has already been written off for accounting purposes in the year of its incurrence but is allowable for tax purposes over a period of time. In this case, the asset representing that expenditure would have a balance only for tax purposes but not for accounting purposes. The difference between balance of the asset for tax purposes and the balance (which is nil) for accounting purposes would be a timing difference which will reverse in future when this expenditure would be allowed for tax purposes. Therefore, DTA would be recognised in respect of this difference subject to the consideration of prudence.

About Author

Jigz Vira

Recommended Articles