as 3, Accounting Standard 3: Cash Flow Statement : The Standard deals with the provision of information about the historical changes in cash and cash equivalents of an enterprise by means of a Cash Flow Statement which classifies cash flows during the period from operating, investing

and financing activities.

- For Companies – As per the Companies Act, 2013, Cash Flow Statement is required to be prepared by every company except a one person, small and dormant company.

- For non-companies – AS 3 is not mandatory for entities falling in Level II and Level III.

Cash comprises cash on hand and demand deposits with banks.

Cash equivalents are short term, highly liquid investments that are readily convertible into known amounts of cash and which are subject to an insignificant risk of changes in value.

⇒An investment normally qualifies as a cash equivalent only when it has a short maturity of, say, 3 months or less from the date of acquisition.

Advertisement

Content in this Article

If you like this article then please like us on Facebook so that you can get our updates in future ……….and subscribe to our mailing list ” freely “

Accounting Standard – 3, Cash Flow Statement (AS 3)

The main reason for the preparation of the Cash Flow Statement is that the Income Statement of an enterprise is always prepared on an Accrual Basis and it may show profits in the Income Statement but the Cash received out of these profits may be low to run the business or vice-versa.

The Cash Flow Statement should report cash flows during the period classified by operating, investing and financing activities

The cash flows associated with extraordinary items should be classified as arising from operating, investing or financing activities as appropriate and separately disclosed.

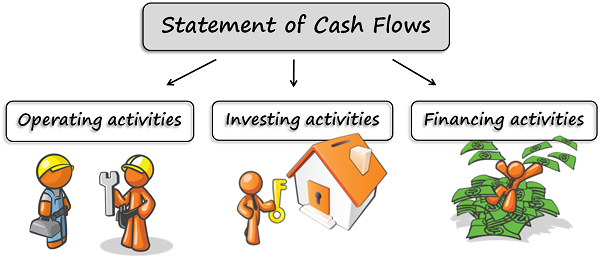

Classification of Cash Flows as per Accounting Standard 3

While preparing the Cash Flow Statement, the cash flows during the period are classified into 3 major categories:-

- Cash Flow from Operating Activities (Direct Method/ Indirect Method)

- Cash Flow from Investing Activities

- Cash Flow from Financing Activities

1. Cash From Operating Activities:

The principal revenue producing activities of a business are called the operating activities of that enterprise. These are the main activities in which it deals. Cash flows arising from these activities are called the cash flows from operating activities. Cash flows from operating activities are the main source of revenue for a business concern. eg. for a company dealing in manufacture of electronics, selling of electronic parts or finished products are the principal revenue producing activities of the concern. For a finance company, giving and taking of loans, purchase and sale of securities are the main revenue producing activities

A. Cash Flow from Operating Activity- Direct Method:

While preparing the Cash Flow Statement as per Direct Method, Actual Cash Receipts from Operating Revenues and Actual Cash Payments for Operating Activities are arranged and presented in the Cash Flow Statement. The difference between Cash Receipts and Cash Payments is the Net Cash Flow from Operating Activities under the Direct Method. In other words, it is a Income Statement (Profit and Loss A/c) prepared on Cash Basis under the Direct Method.

B. Cash Flow from Operating Activity – Indirect Method:

While preparing the Cash Flow Statement as per the Indirect Method, the Net Profit/Loss for the period is used as the base and then adjustments are made for items that affected the Income Statement but did not affect the Cash

2. Cash From Investing Activities:

For carrying out business smoothly, an enterprise acquires long-term assets like machinery, furniture, land, and building. Similarly, old assets are sold and new is purchased. They sometimes also invest idle funds outside the business to get additional earnings. All this results in the inflow and outflow of cash. These flows of cash are termed as Cash flows from Investing Activities.

3. Cash Flows from Financing Activities

Financing Activities are those activities which result in a change in the size and composition of owner’s capital and borrowing of the organisation. The separate disclosure of cash flows arising from financing activities is important because it is useful in predicting the claims on future cash flows by the providers of funds.

Recommended Articles

Thanks for providing me this it is great and helpful. Please provide me notes in INDIAN CONTRACT ACT, 1872.

and other helpful material for my ipcc exams of May 2016

Hi Priyanka You may download Indian Contract Act Notes from following link https://files.caknowledge.com/download/download-indian-contract-act-1872-best-easy-notes/

sir wiil u provide formets of cash flows in both the methods

Hi nandu adimalla

We try to provide as soon possible.