Suspense Account: When a trial balance does not agree, efforts are made to locate errors and rectify them. However, if reason for disagreement of trail

IndAS 2 – The objective of this Standard is to prescribe the accounting treatment for inventories. This Standard provides the guidance for determining the cost

Net Present Value (NPV): Present value of cash flows minus initial investments, The Net Present Value (NPV) method as an investment appraisal or capital budgeting

Ind AS 11, Construction Contracts:Ind AS 11 prescribes the accounting treatment of revenue and costs associated with construction contracts. Because of the nature of the

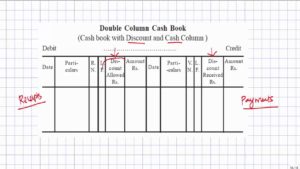

Cash Book -Every business activity ultimately result in cash, therefore, recording of transaction involving cash must be recorded in a separate journal. This journal is

Should Professional Accountants Care about Culture? Yes!.Extensive rules and procedures alone are not enough to ensure appropriate conduct in the work place—the financial crisis of

Ind AS 109, Financial InstrumentsThe objective of Ind AS 109 is to establish principles for the financial reporting of financial assets and financial liabilities that

Meaning of Accounting: According to AICPA Accounting is the art of recording, classifying and summarizing in a significant manner and in terms of money, transactions

Rectification of Errors:Every concern is interested in ascertaining its true profit and financial position at the close of the trading year. But inspite of the

Difference between Capital Receipts and Revenue Receipts: Receipts which are not of revenue nature are capital receipts.The Receipts which are not received now and then

Accounts and its Classification (Accounts Classification): The business transactions are recorded in accounts. An account is an individual record of a person, firm, or thing, an

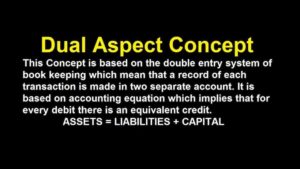

Dual Aspect Concept – Accounting is a language of the business. Financial statements prepared by the accountant communicate Financial information to the various stakeholders for

Accounting Standard 13 – Accounting for investments (AS 13).This Standard deals with accounting for investments in the financial statements of enterprises and related disclosure requirements.

IndAS 7, Statement of Cash Flows:Ind AS 7 prescribes principles and guidance on preparation and presentation of cash flows of an entity from operating activities,

Ind AS 29, Financial Reporting in Hyperinflationary Economies:Ind AS 29 shall be applied to the financial statements, including the consolidated financial statements, of any entity

Ind AS 101, First Time Adoption of IndianAccounting Standards:The objective of Ind AS 101 is to ensure that an entity’s first Ind AS financialstatements, and

Revenue Expenditure:Expenses whose benefit expires within the year of expenditure and which are incurred to maintain the earning capacity of existing assets are termed as

Advantages of Accounting: These advantages usually coincide with the ability for companies to improve operations and overall profitability. Business owners can also create a competitive