Lateral Charge on Ecommerce: All though the above two cases are listed in section 2(98) as ‘reverse charge’, there is another provision which deserves mention in the context of reverse charge. And that provision is the liability of ecommerce operator to pay tax on supply of services through the digital platform or network and for this reason, it can be referred as Lateral Charge as it is neither a forward or reverse charge. This is provided in section 9(5) of the CGST Act, which states:

Lateral Charge on Ecommerce

(5) The Government may, on the recommendations of the Council, by notification, specify categories of servicesthe tax on intra-State supplies of which shall be paid by the electronic commerce operator if such services are supplied through it, and all the provisions of this Act shall apply to such electronic commerce operator as if he is the supplier liable for paying the tax in relation to the supply of such services: Provided that where an electronic commerce operator does not have a physical presence in the taxable territory, any person representing such electronic commerce operator for any purpose in the taxable territory shall be liable to pay tax: Provided further that where an electronic commerce operator does not have a physical presence in the taxable territory and also he does not have a representative in the said territory, such electronic commerce operator shall appoint a person in the taxable territory for the purpose of paying tax and such person shall be liable to pay tax.

The reasons why this provision deserves special mention are:

- It is excluded from the definition of ‘reverse charge’ yet tax is not payable by the supplier

- It is tax payable by a person who is not the recipient but a third person facilitating supply

- It is tax payable not as if the ‘person liable’ to pay tax but as if the ‘supplier liable’ to pay tax

Notification 17/2017-Central Tax (Rate) dated 28 June, 2017 specifies that ‘ecommerce operator’ is liable to pay tax ‘as if he is the supplier liable to pay tax’ and lists the following:

- (i) services by way of transportation of passengers by a radio-taxi, motorcab, maxicab and motor cycle;

- (ii) services by way of providing accommodation in hotels, inns, guest houses, clubs, campsites or other commercial places meant for residential or lodging purposes, except where the person supplying such service through electronic commerce operator is liable for registration under sub-section (1) of section 22 of the said Central Goods and Services Tax Act.

Advertisement

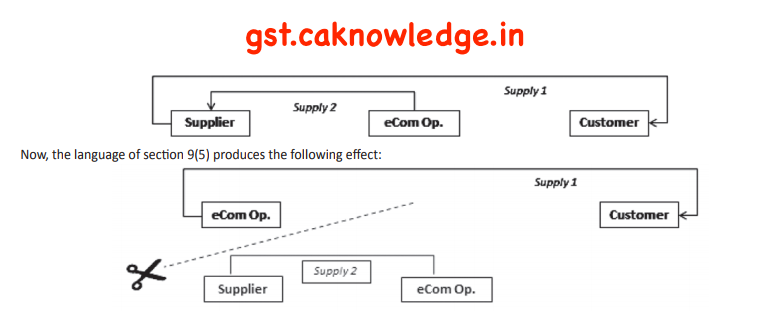

The effect of this language deserves special mention of the following effects that are a departure from section 9(4) to the extent that:

- Not only is the actual supplier not liable to tax (substitutionary effect)

- But also that the supply of services by the ecommerce operator to the actual supplier gets subsumed

Substitutionary effect has been explained earlier in the context of section 9(4) but this ‘subsuming effect’ may be discussed now. There are two supplies involved here, namely:

- Service provided by the actual supplier (taxi driver) to the passenger – taxi service

- Service provided by the ecommerce operator to the actual supplier – commission for securing customer for taxi service

Ecommerce operator having been treated as the ‘supplier liable to tax’ in ‘Supply 1’, he cannot at the same time continue to be treated as a commission agent in ‘Supply 2’. The faction created must be carried through to its ‘purposeful end’ in this provision, that is, Supply 2 would be subsumed into Supply 1. There is no further tax payable on Supply 2 when the entire tax on Supply 1 at the full value is paid by the ecom operator.

Further, on looking into section 24, we find that the actual supplier where section 9(5) applies, is excluded from compulsory registration. In fact, when the tax liability is fastened on the ecom operator, the actual supplier is excluded from registration even if he crosses threshold benefit since section 24 overrides section 22 provided the actual supplier has no other taxable supplies.

IGST-CGST-SGST

The entire discussion above has been based on ‘intra-State’ supplies. With identical provisions appearing in section 5(3), (4) and (5) of IGST Act, the above discussion will apply even in case of ‘inter-State’ supply. In case of tax payable by ecom operator, notification 14/2017-Integrated Tax (Rate) dated 28 June, 2017 applies the tax on inter-State supplies.

Only one aspect to mention here is that when a transaction is an inter-State supply and liable to payment of IGST but not paid, then section 5(4) is attracted. However, if the ‘place of supply’ and ‘location of (unregistered) supplier’ are in the same State, then even though no tax has been paid, section 5(4) cannot apply. The reason being tax that should have been paid is CGST-SGST in another State, if the supplier were to be registered and there was no occasion for that tax to be creditable in any other State. Now, that this transaction is carried out by an unregistered person, tax cannot be collected by a State that could not have collected it had the supplier been registered. Again on this, the last word has not yet been heard but the principle should prevail

Related Articles

- Compulsory payment of GST

- Notification for Reverse charge

- Key points of Reverse Charge

- Reverse Charge under GST

- List of Goods and Services

- GST Reverse Charge

- Reverse Levy on Supplies

- General Reverse Charge

- Specific Reverse Charge